Legal risks can sink a startup. Shielding your business from such threats is vital.

Startups face unique legal challenges. From intellectual property disputes to contract issues, the landscape is fraught with potential pitfalls. Understanding these risks and how to manage them can safeguard your venture’s future. This blog will guide you through essential strategies to protect your startup.

We will discuss common legal risks and practical steps to mitigate them. Early preventive can save time, money, and stress. Whether you’re just starting or already running your business, knowing how to navigate legal waters is crucial. Let’s into how you can keep your startup legally secure and thriving. More

Credit: fastercapital.com

Identify Legal Risks

Identifying legal risks is crucial for protecting your startup. Understanding potential legal issues can save you time, money, and stress. Below, we will explore common legal issues and industry-specific risks.

Common Legal Issues

Several legal issues can affect any startup. Being aware of these can help you take preventative :

- Intellectual Property (IP): you protect your ideas, products, and brand.

- Contracts: Have clear agreements with employees, partners, and clients.

- Employment Law: Comply with labor laws and employee rights.

- Data Protection: Follow regulations like GDPR and CCPA.

- Tax Compliance: Understand your tax obligations to avoid penalties.

Industry-specific Risks

Different industries face unique legal challenges. Identifying these can help you stay compliant:

| Industry | Specific Risk |

|---|---|

| Technology | Software licensing and cybersecurity laws |

| Healthcare | HIPAA compliance and patient confidentiality |

| Finance | Anti-money laundering regulations |

| Retail | Consumer protection and e-commerce regulations |

By understanding these common and industry-specific risks, you can better protect your startup from legal pitfalls.

Credit: fastercapital.com

Choose The Right Business Structure

Choosing the right business structure is crucial for protecting your startup from legal risks. The structure you select will impact your taxes, liability, and paperwork. It is essential to understand the different options to make an informed decision. Here, we will explore some common business structures and their benefits. More update and learn more

Sole Proprietorship Vs. Llc

A sole proprietorship is the simplest business structure. It is easy to set up and manage. However, it does not offer personal liability protection. This means your personal assets are at risk if your business faces legal issues.

On the other hand, a Limited Liability Company (LLC) provides personal liability protection. Your personal assets are separate from your business assets. This structure also offers flexibility in management and tax options. An LLC is suitable for many small businesses seeking liability protection.

Corporation Benefits

A corporation is a more complex business structure. It offers the highest level of personal liability protection. Shareholders are not personally liable for the company’s debts and liabilities.

Corporations can also attract investors more easily. They can issue stocks to raise capital. This structure is beneficial for businesses planning to grow significantly. However, corporations require more paperwork and regulatory compliance.

Understanding these business structures can help you protect your startup. Make sure to choose the one that aligns with your business goals and offers the necessary legal protection.

Draft Clear Contracts

Drafting clear contracts is crucial for protecting your startup from legal risks. Well-drafted contracts help avoid misunderstandings and disputes. They set clear expectations for all parties involved. This section will explore essential contract clauses and the importance of consulting legal experts.

Essential Contract Clauses

Every contract should include essential clauses to protect your startup. First, define the scope of work. This everyone knows their responsibilities. Second, include payment terms. This outlines how and when payments will be made. Third, add confidentiality agreements. This protects sensitive information from being shared. Fourth, include termination clauses. This specifies conditions for ending the contract. Lastly, include dispute resolution methods. This offers a clear way to resolve conflicts without going to court.

Consulting Legal Experts

Consulting legal experts is vital for drafting clear contracts. Lawyers understand legal language and can help avoid potential pitfalls. They your contracts comply with all relevant laws. Legal experts can also help customize contracts to fit your startup’s needs. They review and update contracts as needed. Having a lawyer review contracts can save your startup from costly legal issues.:max_bytes(150000):strip_icc()/terms_i_intellectualproperty_asp-FINAL-f1e432ec66da49fe9ce0177ddf0d9166.jpg)

credit: inverstopedia.com

Protect Intellectual Property

Protecting your startup’s intellectual property is crucial. It safeguards your unique ideas and innovations from being copied. This involves several key steps, including trademark registration and patent protection. Let’s into these areas to help secure your startup’s future.

Trademark Registration

A trademark protects your brand’s identity. It includes your company name, logo, and slogan. Learn about it Clerky Pricing And Features a trademark gives you exclusive rights to use them. This prevents others from using similar marks that could confuse customers.

Here are steps to register a trademark:

- Conduct a trademark search to uniqueness.

- Fill out the application form on the official trademark website.

- Submit the form and pay the required fee.

- Wait for the approval process to complete.

Patent Protection

Patents protect your inventions. They give you the right to exclude others from making, using, or selling your invention. This protection is vital for innovative products and technologies.

To obtain a patent, follow these steps:

- Conduct a patent search to check if your invention is unique.

- Prepare a detailed description of your invention.

- File a patent application with the relevant patent office.

- Pay the necessary fees and wait for the review process.

Protecting your intellectual property is an ongoing process. Regularly monitor the market for infringements. Take legal action if necessary to protect your rights.

Comply With Employment Laws

Your startup complies with employment laws. This helps avoid costly legal issues and protects your business. Stay informed and follow regulations.

Understanding employment laws is crucial for your startup. Non-compliance can lead to fines or legal action. It also protects your employees’ rights. This builds trust and a positive workplace environment. Let’s into two key areas: employee agreements and workplace policies.

Employee Agreements

Create clear and detailed employee agreements. These should outline job roles, responsibilities, and compensation. Include confidentiality clauses to protect your business information. Non-compete agreements can prevent employees from joining competitors. all agreements comply with local laws. This can prevent disputes and misunderstandings.

Workplace Policies

Develop comprehensive workplace policies. These should cover attendance, behavior, and safety. Policies help maintain order and set expectations. Make sure employees read and understand these rules. Regularly update policies to reflect changes in the law. This keeps your business compliant and your employees informed. “`

Ensure Data Privacy

Ensuring data privacy is crucial for every startup. It builds trust and protects your reputation. Mishandling data can lead to severe legal consequences. Here are steps to data privacy for your startup.

Data Protection Laws

Understanding data protection laws is essential. Different regions have different laws. Familiarize yourself with regulations like GDPR, CCPA, or HIPAA. Non-compliance can result in hefty fines.

- GDPR: General Data Protection Regulation in the EU.

- CCPA: California Consumer Privacy Act in the US.

- HIPAA: Health Insurance Portability and Accountability Act in the US.

your data practices align with these laws. Regularly review updates and changes to regulations.

Customer Data Security

Protecting customer data is. Implement strong security measures. Use encryption to safeguard data. Regularly update your software and systems.

- Encrypt sensitive data.

- Use secure passwords and multi-factor authentication.

- Regularly update software and systems.

- Conduct regular security audits.

Have a clear data breach response plan. Train your employees on data security best practices. This everyone understands their role in protecting data.

Consider using a table to outline key data security measures:

| Measure | Description |

|---|---|

| Encryption | Secures data by converting it into a code. |

| Secure Passwords | Use strong, unique passwords for all accounts. |

| Software Updates | Regularly update to patch vulnerabilities. |

| Security Audits | Regularly review and test your security measures. |

By following these steps, you can protect your startup from legal risks related to data privacy.

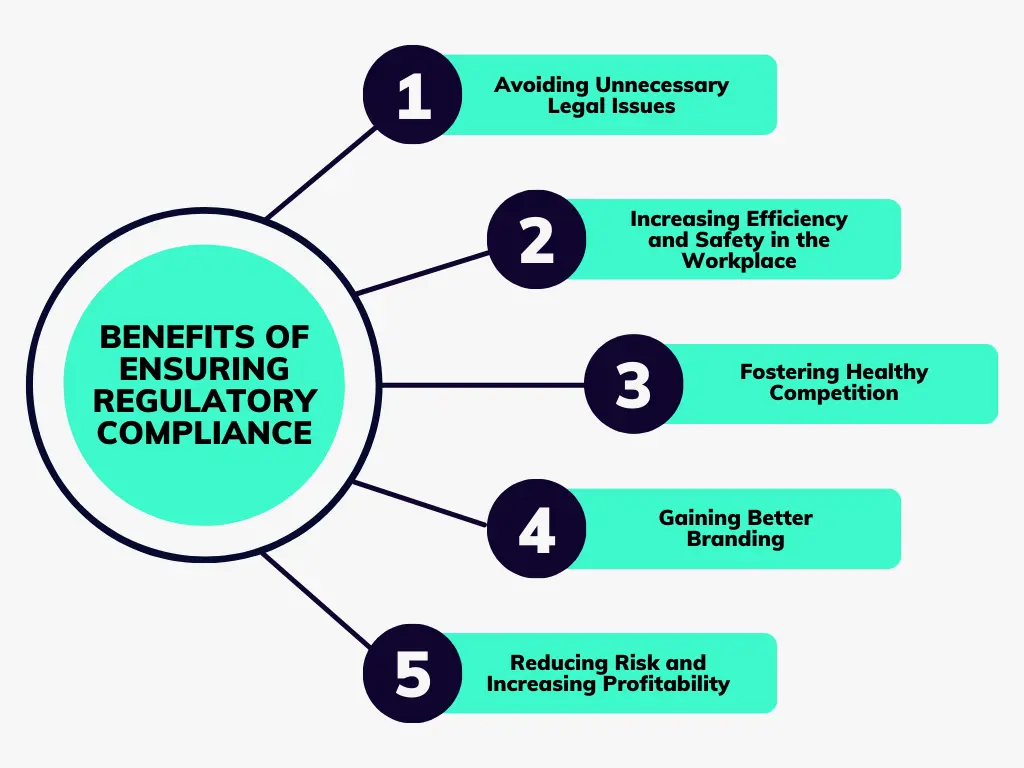

Maintain Regulatory Compliance

Maintaining regulatory compliance is crucial for protecting your startup from legal risks. It helps that your business operates within the law. This is not only important for avoiding fines but also for building trust with customers and investors. Let’s explore some key areas to focus on.

Industry Regulations

Understand the specific regulations that apply to your industry. Different industries have different rules. For example, healthcare startups must follow HIPAA guidelines. Financial businesses need to comply with regulations like GDPR. Knowing these rules helps you avoid costly mistakes.

Regular Compliance Audits

Conduct regular compliance audits to check if your startup follows all regulations. These audits help identify any gaps in your compliance efforts. Fixing these gaps can save you from legal trouble. Regular audits also show that you are proactive about compliance.

Credit: thesocialmedialawfirm.com

Plan For Dispute Resolution

Protecting your startup from legal risks involves many steps. One crucial step is to plan for dispute resolution. Disputes can arise at any time and from any direction. Having a plan in place can save your startup time, money, and stress. Let’s explore the different methods for resolving disputes, including mediation, litigation, and arbitration clauses.

Mediation Vs. Litigation

Mediation and litigation are two common ways to resolve disputes. Each has its own benefits and drawbacks.

Mediation is a voluntary process. Both parties work with a neutral third party, the mediator. The mediator helps them reach a mutual agreement. Mediation is usually quicker and less expensive than litigation. It also allows for more flexible solutions.

Litigation, on the other hand, involves going to court. A judge or jury makes the final decision. Litigation can be long and costly. It is often seen as a last resort. The outcome is less predictable, and relationships can be damaged.

Here is a quick comparison:

| Aspect | Mediation | Litigation |

|---|---|---|

| Cost | Lower | Higher |

| Time | Shorter | Longer |

| Control | Parties have more control | Court has control |

| Outcome | Flexible | Fixed |

Arbitration Clauses

Arbitration clauses are another option for dispute resolution. These clauses are included in contracts and require disputes to be resolved through arbitration.

Arbitration involves a neutral third party, the arbitrator. The arbitrator listens to both sides and makes a decision. The decision is usually binding. Arbitration is often faster and cheaper than litigation. It also offers more privacy.

When drafting contracts, consider including arbitration clauses. This can a smoother and quicker resolution process.

Frequently Asked Questions

What Are Common Legal Risks For Startups?

Startups often face risks like intellectual property disputes, contract breaches, and compliance issues. Identifying these risks early is crucial. Proper legal frameworks can help mitigate these risks effectively.

How Can Startups Protect Intellectual Property?

Startups should secure patents, trademarks, and copyrights. These protections prevent others from using their ideas. Consulting with an intellectual property lawyer can be beneficial.

Why Is Legal Compliance Important For Startups?

Legal compliance prevents fines and penalties. It the business operates within legal boundaries. Staying updated with regulations is essential for long-term success.

How To Choose A Good Startup Lawyer?

Choose a lawyer with experience in startup law. Look for recommendations and reviews. they understand your industry and business needs.

Conclusion

Protecting your startup from legal risks is crucial. Start with proper legal advice. Create clear contracts for all parties. Regularly review and update legal documents. Stay compliant with regulations. Educate your team on legal matters. Prioritize intellectual property protection. Address potential risks early.

Being proactive saves time and money. Your startup’s future depends on it. Stay informed and prepared. Legal stability leads to business success. Take action now.